Volume 2, Issue 4

The Influence of Early Gendered Messages in the Household and Broader Society on Women’s Financial Literacy and Investment Behaviors Later in Life

By Malimi Fernando and Gabriella Osorio

is a fourth-year Marketing Analytics and Finance major. Their research area focuses on gender inequality, with a focus on the gender wealth gap. Her research advisors are Dr. Melinda Adnot from the Honors College, Dr. Jennifer Ames Stuart from the Department of Marketing, Dr. Stephanie Bradley from the Department of Sociology, and Dr. Gene Lai from the Department of Finance.

is a fourth-year Biology major, with a minor if Child & Family Development. Her research area focuses early socialization and its influence on females’ views of their place and capabilities in society. Her research advisors is Dr. Jennifer Ames Stuart from the Department of Marketing.

Abstract

There is a financial gender gap, specifically in investing, that can be traced back to differences in financial literacy and the effects of early socialization. Early socialization refers to household and societal messages that shape children’s beliefs, confidence, and behavior. This literature review synthesizes evidence linking early gendered socialization to later financial literacy differences and investment behavior. The review examines early socialization, specifically the development of internalized sexism through influences such as parental roles, societal norms, linguistic structures, and exposure to benevolent sexism and explores gender differences in adults’ financial attitudes, literacy, and behavior. These areas are connected through the potential influence of internalized sexism on confidence and self-competency. The reviewed studies suggest that early gendered messages and unequal exposure to financial education contribute to women’s lower investment participation compared to men, as well as their confidence and risk tolerance in investing, reinforcing the financial gender gap observed in adulthood. The implications of this research are to increase awareness of how early gendered messaging shapes women’s financial confidence and investment participation across their lifespan, while also highlighting the importance of representation shifts and informing future financial literacy education policy and intervention efforts.

Gendered socialization, Linguistic relativity theory, Benevolent sexism, Internalized sexism, Financial literacy, Investment behaviors, Risk, Confidence

Introduction

Extant research finds that early socialization may shape women’s financial literacy and investment behaviors including participation in financial markets, asset allocation choices, risk tolerance, and engagement with financial advice later in life. This review evaluates how the development of internalized sexism through exposure to gender-verbiage and expectations in society can greatly influence these behaviors. There is a lack of research on the direct connection between early socialization and financial behaviors later in life; however, this review aims to draw a connection for further research. Sexism is defined as behaviors, beliefs, or attitudes that support the unequal status of women and men ( Swim & Campbell, 2001). While sexism can operate at institutional, interpersonal, and internalized levels (Bearman & Amrhein, 2014; Cudd & Jones, 2005) this review focuses intensely on internalized sexism. Internalized sexism refers to a form of internalized oppression, whether it is a specific value, belief, rule, or behavior, and sustaining it as a characteristic of themselves, which often includes adopting the prejudices of society towards the stigmatized group (Herek, 2009). Internalized sexism reveals how women can maintain the norms of a patriarchal system, just as much as men, through their own beliefs and actions (Hooks, 2018). Croft and colleagues (2015) explained how internalized sexism diminishes one’s personhood by limiting their sense of who they should be or who they could become. Regardless of the numerous opportunities society promotes to solve the gender inequality issue in today’s world, the “glass ceiling” in society still exists, partially due to the internalized beliefs of women that limit their self-confidence and feelings of self-competency. Early gendered messaging in households and society may greatly contribute to differences in women’s financial literacy and investment behaviors. This review therefore (1) examines how early gender socialization contributes to internalized financial beliefs, (2) evaluates gender differences in financial literacy across development, and (3) analyzes how these differences influence investment behavior across the life course. This review contributes to the literature by synthesizing developmental, linguistic, and socialization pathways linking early gendered messaging to later financial literacy and investment participation.

Although prior research has examined gender differences in financial literacy and investment behavior, fewer studies directly connect early gender socialization processes to later financial outcomes. This paper evaluates previous studies that discuss sexism, linguistic relativity theory, and parental influence for early socialization through a broader lens and explores how these factors play into the disparity of financial literacy between men and women and how that may contribute to gendered differences in investing patterns. The contribution of this research is to acknowledge the gender socialization differences in development that women experience and their impact on financial literacy and investment behaviors later in life and initiate the conversation towards finding solutions to improve performance in financial fields, namely investing. While the focus demographic for this review is middle-class men and women, specifically children, adolescents, and young adults, it is important to note that several other demographics may have differing experiences, including differences related to marital status or income and socioeconomic status.

Financial literacy affects how one invests, and studies show a gender difference in investment behaviors between men and women — a topic important to understand in today’s context. Financial literacy is defined as: “The ability to read, analyze, manage, and communicate about the personal financial conditions that affect material well-being. It includes the ability to discern financial choices, discuss money and financial issues without (or despite) discomfort, plan for the future, and respond competently to life events that affect everyday financial decisions, including events in the general economy” (Vitt et al., 2000).

As AI and other technological tools increasingly impact people’s real-life decisions, such as financial planning decisions, it is essential to understand how societal biases may influence how these tools provide advice. Large language models (LLMs) such as ChatGPT rely on social “rules” in language and speech to differentiate their communication and results based on the receiver’s demographic characteristics, like gender. When there is a societal norm in speaking of areas such as finance as a male-driven subject, AI follows these patterns, replicating real life. Thus, the impact of gendered messages in the household and broader society is far from being a theoretical or historical issue; it is one with real and evolving implications in today’s world.

Methods

This literature review synthesized peer-reviewed research examining gender differences in financial literacy and investment behavior, with attention on the role early gendered socialization plays. Articles were identified using databases including Google Scholar, JSTOR, and PubMed. Search terms included combinations of “financial literacy gender gap,” “investment behavior gender differences,” “development of internalized sexism,” “early gendered socialization,” and “financial advice.” Priority was given to articles published within the past 10–15 years, though foundational studies were included where relevant.

Because financial literacy is defined and measured differently across studies, this review relied on two commonly used models to guide interpretation. The first model focuses on knowledge of financial decision making concepts as opposed to behavior (Bucher-Koenen et al., 2017), while the second incorporates financial attitude, financial behavior, as well as general financial knowledge within a multidimensional framework (Potrich et al., 2017). Together the models provided a consistent conceptual framework for interpreting how financial literacy was defined across the literature included in this review.

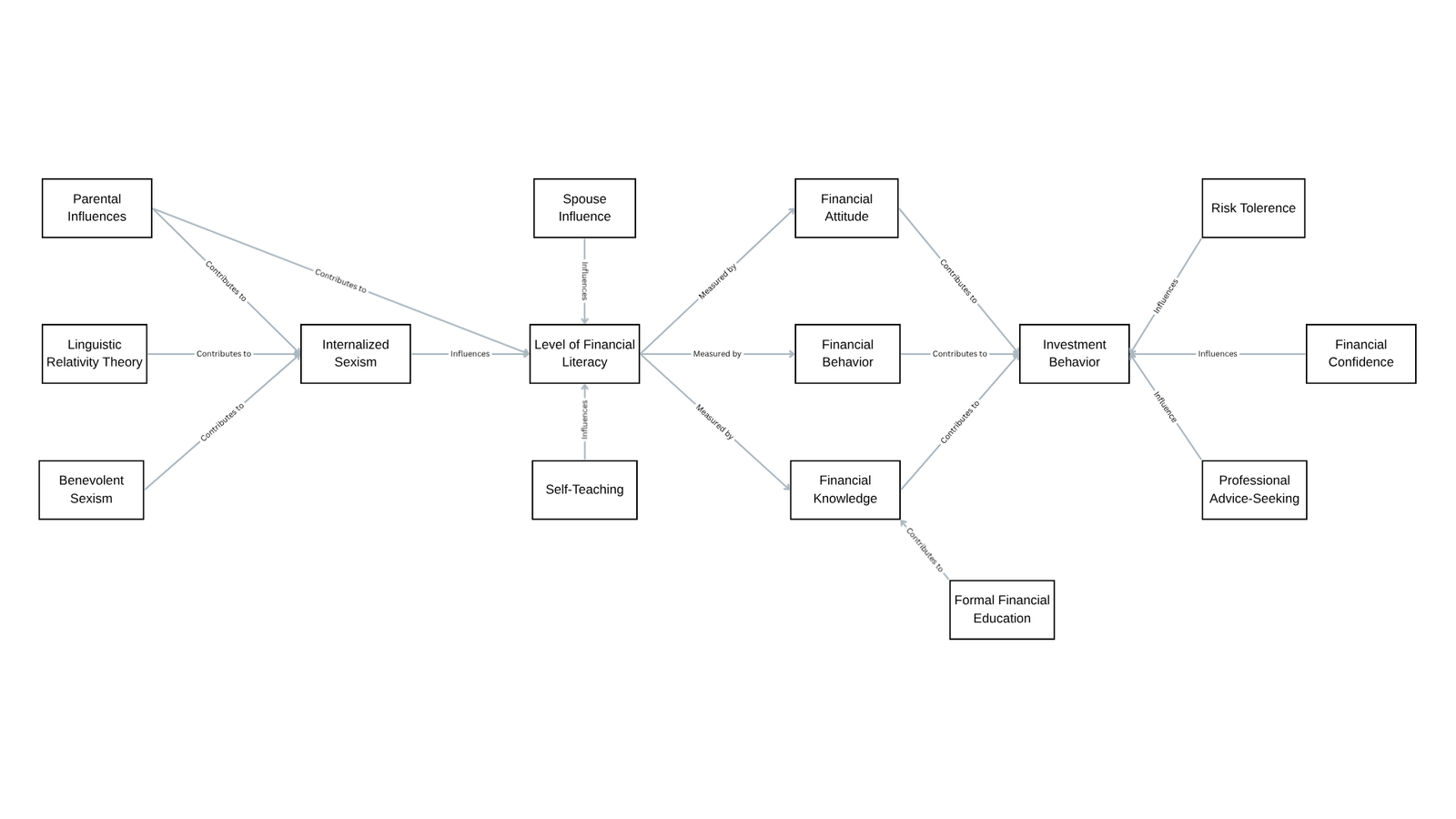

Figure 1: Conceptual map of the research idea.

The diagram shows the contributors to the formation of internalized sexism including benevolent sexism, linguistic relativity theory, and parental influences. It illustrates the influences of an individual’s financial literacy, as well as the measurements of financial literacy. The diagram further depicts the contributors and influences of individuals’ investment behavior. This conceptual map is meant to guide the reader along the concepts presented in this research.

Internalized Sexism and Early Socialization

Early socialization plays a large role in shaping a child’s beliefs about their own ideas of self-competence, risk-taking, and financial decision-making. This section dives into how internalized sexism, benevolent sexism, linguistic structures, and parental influences interconnect to contribute in the development of biased financial beliefs from childhood through early adulthood. Understanding these processes may help explain how gender differences in financial literacy and investment behavior may be seen clearly later in life.

Internalized Sexism

Many factors influence the formation of internalized sexism in women. Due to the consistent repeated exposure to gendered messages across institutions like media, education, and family, individuals may come to internalize sexist beliefs that align with broader cultural norms. Often, people come to internalize dominant ideologies without conscious awareness and this specifically reflects the strength of socialization and systemic power. A previous study on the process of internalizing sexism revealed the existence of both direct and indirect relationships between traditional gender roles, accepting external influences, and self-alienation (Bozkur & Şahin, 2022). Becoming aware and understanding these relationships is of grave importance, precisely because of how women may subconsciously aid in the reproduction of stereotypical messages regarding traditional gender roles (Bozkur & Şahin, 2022). The reproduction of these messages may suggest an enhancement of their own internalized oppression through personal exposure, as well as increasing the exposure of said sexist messages to the women around them. An example of this is the implicit influence mothers can have on their daughters through the reproduction of messages from their own internalized oppression. This implicit influence is supported by previous studies indicating a positive relationship between an individual’s internalization of cultural beliefs about gender roles and the adoption of gender ideology perceived by one’s parents (Bishop, 2017; Jasser, 2008; Jones, 2014; Wenzel & Lucas Thompson, 2012). The formation of this internalized sexism can be due to societal influences just as much as parental influences.

Benevolent Sexism

The ambivalent sexism theory states that there are two interrelated ideologies of prejudice towards women: hostile sexism and benevolent sexism (Glick & Fiske, 1996). When people use the word sexism, most people first think of hostile sexism, which is when women are viewed in a more negative light; they are overly emotional and incompetent, and they are attempting to manipulate men to gain power (Gutierrez et al., 2020). Benevolent sexism, on the other hand, is the ideology that characterizes women as delicate, pure, and in need of men’s protection and care (Gutierrez et al., 2020). In previous studies, benevolent sexism has been linked to decreased cognitive performance, self-esteem, and feelings of competency for women, which suggests a connection to the lack of confidence women experience in investment and finance fields.

The development of benevolent sexism can be seen in early ages through the idea of heroes and the helpless (Hammond et al., 2018). Stereotypical attitudes regarding roles for one’s gender may be present in early childhood, and the development of female-helpless and male-heroic attitudes evolves differently over time (Hammond et al., 2018). Children between the ages of 7-11 start to recognize and internalize components of benevolent sexism. Hammond et al. (2018) revealed that boys across all ages believed that boys should be heroes; however, this bias decreased with age. Simultaneously, as boys grew older, they were more likely to say girls deserve preferential treatment and were less likely to say boys should receive it. Men’s benevolent sexism followed a positive linear trajectory and tended not to change over time. However, this consistent appeal to men could be due to the romantic appearance or how benevolent sexism subtly maintains men’s power (Hammond et al., 2018). On the other hand, girls between the ages of 7-11 showed a significant decrease in endorsing the idea that girls should be placed on a pedestal. This decrease may be due to their increased awareness of gender inequality. Girls’ internalized beliefs develop in a U-shaped trajectory where girls’ endorsement of benevolent sexism may decline in middle childhood but then rise again in adolescence as societal influences shift, suggesting a possible connection to the romantic appearance men are attracted to as well. Although sexism levels were high in the youngest cohorts, the decrease in endorsement of sexist attitudes over time suggests that early awareness efforts may be effective, especially given how flexible beliefs are at a young age (Hammond et al., 2018).

Men and women experience benevolent sexism towards women entirely differently. Benevolent sexism is linked to men helping women in ways that foster dependence on men, which has also been found to be associated with decreased support for gender equality (Gutierrez et al., 2020). Higher accounts of women’s benevolent sexism are connected to life stages where women are making larger financial decisions, including higher education, careers, and establishing serious relationships (Hammond et al., 2018). These stages in a woman’s life are typically when she should be investing; however, due to the increased levels of benevolent sexism, there is a lack of self-confidence when making financial decisions. However, another study finds a positive correlation between levels of benevolent sexism when in relationships and a woman’s tendency to take financial risks (Teng et al., 2021). From these connections, it can be predicted that when a woman is in a relationship with higher levels of benevolent sexism, she takes more financial risks due to the financial support that gives her confidence (Teng et al., 2021). This is a counterargument due to the fact that benevolent sexism is showing an increase in a woman’s confidence rather than a decrease. This could possibly convey that women who are single/not married experience a more negative effect of benevolent sexism while women in relationships could experience a more beneficial effect of benevolent sexism. There is a lack of research in this specific relationship between the factors of relationship status and financial risk taking therefore this phenomenon will not be focused on in this literature review.

Linguistic Relativity and Gendered Messaging

The structure of languages which are used to communicate these gendered societal expectations, including benevolent sexism, may also influence how women internalize them, ultimately impacting their financial literacy and investment behaviors later in life. Linguistic relativity theory describes how the structure of languages plays a distinct role in shaping the thoughts of their speakers and forming an individual’s experience. The underlying premise of this theory is that when a language uses gender differences, individuals are more likely to distinguish between males and females in everyday phrases (Siewierska, 2016). English has a sex-based system, meaning the language’s gender system is linked to a biological sex, and it utilizes gender-differentiated pronouns in the third-person singular for he and she (Hechavarría et al., 2017). The use of gendered verbiage and gender-differentiated pronouns when discussing careers, specifically in investing or finance, can foster the development of internalized sexism in a child through exposure to stereotypes in that specific society (Hechavarría et al., 2017; Boroditsky, Schmidt, & Phillips, 2003). These internalized stereotypes of society through the linguistic relativity theory support the hypothesis of gendered linguistic structures being a predictor of women staying away from investing due to this internal belief that it is not meant for them, thus creating and reinforcing gender stereotypes and inequalities (Cameron, 1998; Prewitt-Freilino et al., 2012).

Parental Influence and Early Financial Socialization

The language parents use subconsciously can have an implicit influence on their children. For instance, the literature supports that mothers influence their daughters through the reproduction of messages from their own internalized sexism, which may have partially been formed by the gendered linguistic structure of English (Jones, 2014; Jasser, 2008). Not only parental language but parental characteristics and their roles in the household hold an exceptionally significant influence on a child’s development of internalized sexism. Focusing specifically on the parental influence on financial literacy, previous studies convey how parents can influence how their children view financial matters. It is critical to note that children internalize the transmission of financial values, norms, and behaviors from their parents, which all contribute to the child’s economic well-being, defined as their developing understanding of money, financial attitudes, and confidence in managing financial decisions shaped through early household experiences (Ranyard, 2018). Whether these lessons are passed down intentionally or unintentionally, teaching specific financial knowledge and applying the particular knowledge can foster feelings of self-confidence and competence in managing finances independently (Ranyard, 2018).

Gender Differences in Financial Literacy

Financial literacy is an essential component in determining decision-making regarding monetary issues. It strongly predicts retirement planning, wealth, and investment outcomes. Notably, individuals who are more financially literate are more likely to participate in the market, which contributes to higher returns (Lusardi et al., 2023). Lusardi et al. (2017) also found that in the United States, lack of financial literacy can be attributed to 30-40% of wealth inequality at retirement. The implications of improvement in financial literacy are immense, as it plays a critical role in shaping economic well-being and reducing wealth disparities. A lack of financial knowledge limits individuals’ ability to make informed financial decisions and contributes significantly to long-term economic inequality.

One fundamental aspect of financial literacy that demands deeper attention is the large disparity in financial literacy between men and women. Potrich et al. (2017) conducted a study following the structure of the second model discussed previously that indicated an equal difference (12.8%) in lower and higher levels of financial literacy between men and women. Bucher-Koenen et al. (2017) utilize a different approach to understanding financial literacy in men and women—the model aimed to understand participants’ basic understanding of interest rates, inflation, and risk diversification. The results of the study found that more men (55%) correctly answered questions related to interest rates and inflation compared to women (38%), and fewer women (22%) answered all three questions correctly compared to men (38%). The study further compared financial literacy among men and women in the United States, the Netherlands, and Germany and found that similar patterns prevailed. These results reveal that women are less financially literate than men, identical to the results of the study conducted by Potrich et al. (2017).

Gender Differences Across Development

The developmental and social influences from an early age that shape financial literacy are essential to consider to understand the root of this persistent gender gap. Financial literacy must be introduced and taught during development to increase the likelihood of success in retirement planning, investing, and other financial decision-making. Parents are the primary influencers of financial literacy, while self-teaching or a spouse is a secondary influence (Clarke et al., 2009). Particularly for women, the significant influence of a spouse can be understood through the lens of internalized and benevolent sexism. As many women are socialized to perceive financial management as a male responsibility, they may defer to their partners due to internalized beliefs about their own financial incompetence. Benevolent sexism further reinforces this dynamic by framing men as natural providers and protectors, subtly discouraging women from independently developing financial literacy. Clarke et al. (2009) also discuss that practicing financial tasks and thoroughly teaching finances at home, rather than outside, makes adolescents feel more financially prepared. However, perceived parental influence significantly impacts financial attitude, not financial knowledge; it also indirectly influences financial behavior, mediated through financial attitude (Jorgensen et al., 2010). A study also found that males have their first financial discussion in the home at a younger age than females on average, which suggests that financial socialization in the home may be subject to a gender bias, over time contributing to differing financial literacy knowledge levels between the genders (Agnew & Cameron‐Agnew, 2015). Thus, financial attitude/preparedness, which influences financial behavior, is highly influenced by parents during development. Parents harboring gendered biases might then significantly impact the financial literacy of their children, particularly in girls.

The most common form of indirect parental economic socialization is through role modeling. Children learn about money and financial behavior best by observing and imitating the most relevant models (Ranyard, 2018). Variables such as the parents’ highest level of schooling and a mother’s presence in the household were positively correlated with a student’s financial knowledge (Chambers et al., 2019). Agnew (2015) found that students attending medium decile schools had the smallest difference between male and female roles. Low socioeconomic families tended to see males as more likely to be the predominant breadwinner, indicating a more extreme view of gender roles. The largest difference in gender stereotypes in homes around financial literacy was when the students were asked to say which parent influences how they spend their money. Students across genders were more than twice as likely to answer that their father had the biggest influence. These findings emphasize the traditional stereotypes around the father being more financially knowledgeable than the mother and playing a larger role in financial discussions than the mother.

Moreover, parents explicitly teaching children and adolescents about finances better aids women in making more informed financial decisions than men. A study by Jorgensen et al. (2010) found that both men and women had better financial attitudes if they believed they were explicitly taught about finances by their parents. Still, women who were perceived to have explicitly learned about finances from their parents had higher financial behavior scores than men. Furthermore, although students expect to learn financial knowledge from their parents, parents may not explicitly teach it to their children (Jorgensen et al., 2010), as parents might view financial literacy as something to be taught in school rather than in the household. Teaching financial literacy during development is especially important for women, as women report feeling less financially prepared for tasks such as investing than men, even when mothers significantly model investing (Clarke et al., 2009). This gender gap in financial attitude suggests that financial teaching in households, beyond simply modeling financial behaviors, is crucial for women to feel more confident in the topic and increase future engagement, such as investing.

In addition to family influence, financial education is another critical factor for improving financial knowledge in both men and women and helping close the gender gap in financial literacy. Goldsmith et al. (2006) found that while neither men nor women are adequately financially literate, men scored higher on real investing knowledge than women. Men’s subjective knowledge of investing was also higher than women’s. However, the study found that this gap in perceived financial/investing knowledge virtually disappeared when students were given formal education through a Family Financial Analysis Finance course. Through this course, both men and women substantially increased real investment knowledge. This study proves that consumer education increases financial literacy and decreases the responsible financial behavior gap between men and women, as financial knowledge in women increases (Tang et al., 2015).

Impact on Investment Behavior

Risk Tolerance

Financial literacy is crucial in developing optimal investment strategies, and men and women differ in their choices when deciding which personal investment option to invest in. Men prefer to invest in risky investments such as common stocks and real estate investments, while women prefer to invest in funds, time deposits, and gold (Bayyurt et al., 2013). Ulifalean (2024) also found that women prefer bank deposits more than men (by 23.21%), as bank deposits are considered low-risk investments. The risk of losing that money due to a personal choice is eliminated with bank deposits, making it an enticing option for women. Contrary to the findings of Bayyurt et al. (2013), however, Ulifalean (2024) found that men do prefer funds more than women (by 23.81%). Both studies agree that men prefer to invest in stocks more, which is arguably one of the riskiest investments. However, there is an equal preference between men and women for bonds, which Bayyurt et al. (2013) identified as one of the riskier investment options. While women preferred bank deposits, it was considered one of the least popular options among men, alongside savings accounts (Ulifalean 2024). These findings align with the argument that women prefer low-risk investments that generally require less knowledge of finance and market fluctuation.

Gender differences in risk tolerance can be linked to early financial socialization in women. Women are likely first exposed to financial learning opportunities in college, where they have exposure to more financial learning opportunities than men (Tang et al., 2015). Female college students also have more conversations about finances with their parents than males (Tang et al., 2015; Edwards et al., 2007). Interestingly, Edwards et al. (2007) found that higher financial dependency contributes to more conversations with parents on financial learning. Nevertheless, these studies found that young women are still less likely to take financial risks and tend to have more anxiety about finances. This implies a gender difference in how parents socialize women regarding finance, in that young women do not get many financial learning opportunities until college. When they inquire about finances with their parents, women potentially receive advice to be more conservative with their finances.

Confidence and Participation

Early financial socialization and women’s patterns of risk-aversion suggest that gendered messages in the household may strongly influence women’s financial confidence. According to a survey study by Gill and Biger (2009), women’s perceived lack of financial literacy is the most significant factor contributing to the disparity in investment decisions. The study reveals that women often view themselves as less financially knowledgeable, which may affect their investment behavior. Crost et al. (2015) highlight that internalized sexism limits one’s sense of self by diminishing personhood, entailing that women who have internalized differing forms of sexism might view themselves as incapable of male-dominated activities such as investing. Therefore, lack of confidence in their financial expertise might stem from internalized sexism, a result of various social factors, most notably the exposure to benevolent sexism. These findings align with previous research, emphasizing the role of gendered perceptions in shaping financial decisions.

Thus, a lack of confidence in financial literacy contributes to gender differences in personal investing. Men tend to be overly confident in matters regarding finance, as finance is generally seen as a more male-dominated industry. Furthermore, growing research suggests that this is due, in part, to the fact that men are more exposed to financial matters and losses in early development (Blaschke, 2022). A study observing self-confidence in respondents’ financial literacy and measuring financial literacy found a gender gap in the reported self-confidence and the number of participants holding risky assets. Results indicated that men tend to be more confident in their financial abilities and obtain higher scores in financial literacy across several countries. Individual confidence in men tends to be a significant predictor of holding risky assets, as stated by Cupák et al. (2020).

Long-Term Financial Outcomes

Overconfidence in financial literacy also contributes to unsuccessful returns, as overconfidence steers towards higher trades and lower expected utilities (Barber & Odean, 2001). Due to men being more confident in finance, men tend to trade more than women, leading to excessive trading. Overconfident investors believe in their ability to accurately assess securities’ values, which yields unrealistic expectations of how high their returns will be (Barber & Odean, 2001). High trading frequency has been seen to lower investors’ returns, and buying and holding an investment leads to better returns (Willows et al., 2015). Specifically, trading less leads to higher long-term returns, and single men trade 67% more than single women (Barber & Odean, 2001). Thus, a degree of risk aversion and healthy financial confidence driven by high financial literacy is needed to make the best informed financial decision.

Further, studies find that knowing when to be more confident and risky and when to be more conservative in one’s investments could potentially hold strong returns for investors. During the 2008 through 2009 financial crisis in South Africa, women outperformed men in trading/investing; after the crisis, however, men invested better (Willows et al., 2015). This suggests that since women are more conscious of where and when they invest their money, it may serve as an advantage during an economic crisis when reducing risk-taking is advised. Men might be seen as better investors after an economic crisis, as it is better to be more risk-tolerant and confident when the economy is recovering from such a crisis.

Gendered Financial Advice and Decision Support

Given the gendered messages that women receive throughout their development, which affect their investment behavior, it is also important to examine how investment advice-seeking in adulthood may reinforce or challenge these messages. As there are significant differences in how men and women invest, it is advisable for financial advisors to tailor their approach based on their clients’ gender. However, this does mean that men who harbor pre-existing biases regarding gender may provide biased advice to women on how they should invest. A study found that financial planning firms, as opposed to securities firms, give suboptimal advice to female clients based on gender, particularly if they indicate lower risk tolerance, lower confidence, and a domestic outlook (Bhattacharya et al., 2024). This is because if an advisor already has preexisting biases and holds either hostile or benevolent sexist ideologies, they tend to offer gendered financial advice. Interestingly, a study also found that large language models such as ChatGPT offered gendered recommendations based on whether they perceived the profession as masculine or feminine. They provided less risky, prevention-oriented recommendations to female professions, and texts written to women had a patronizing tone and were more simplified than those written to men (Etgar et al., 2024). These findings suggest that gender biases in investing can manifest in AI-driven recommendations alongside financial advisors, thus aligning with the idea that preexisting biases can be tied to systematically different financial guidance based on the receiver’s gender.

Moreover, parental socialization influences financial advice-seeking habits in women. Simms (2014) found that only 24% of women reported using investment advice in the past five years since the study was conducted. In the findings, women were labeled as either “strugglers” or “thrivers,” with lower self-assessed risk aversion being one crucial distinguishing factor between the two groups. The study found that “thrivers” are less likely to seek financial advice when someone in the household knows more about finances than they do. Thus, risk tolerance is crucial in predicting whether a woman will seek financial advice. Such advice-seeking behavior is indirectly tied to parental style and whether one received an allowance during development; it is also directly tied to financial literacy and risk tolerance. Receiving an allowance during adolescence is associated with a greater financial risk tolerance, and higher levels of financial knowledge and risk tolerance are correlated with a higher likelihood of seeking professional financial advice (Fan et al., 2021). Therefore, early financial experiences through parental socialization contribute to the development of financial confidence and a willingness to seek professional advice — factors that influence the gender gap in investing and finance.

Discussion

The literature suggests that early gendered messaging may shape internalized beliefs about financial competence, which influence financial literacy development and ultimately contribute to financial behavior and investment participation patterns across adulthood. There is a disparity in financial literacy between men and women based on tests of financial knowledge, attitude, and behavior. Financial literacy is a determinant of investment patterns, as a lack of financial literacy, or perceived lack thereof, can contribute to less financial confidence in women. Financial confidence is tied to risk tolerance in investing, and men have been found to prefer to invest in riskier investments than women. Moreover, women’s lack of financial confidence can be linked to experiencing benevolent sexism, as it is correlated with decreased cognitive performance, self-esteem, and feelings of competency for women. Because financial literacy develops early in life, parental socialization plays a central role in shaping these confidence differences across development. Several studies have found that direct financial education by parents is crucial in determining a child’s financial literacy later in life (Clarke et al., 2009; Jorgensen et al., 2010), as parental characteristics and roles significantly influence the development of their children’s mindsets. Children who learn about finances from parents tend to have more financial knowledge and better financial behaviors later in life. However, males have financial discussions at home at a younger age than females, suggesting gender biases in financial education in the home. Linguistic relativity theory, the idea that languages with gender-differentiated structure may create and reinforce gender stereotypes and inequalities, may then explain why women tend to invest less, or be more risk-averse, than men. These findings suggest that gender differences in financial behavior are not only shaped by access to financial knowledge but also by early socialization processes that influence confidence, perceived competence, and participation across the life course.

Limitations

There are, however, limitations to this work. Financial literacy is patterned by many demographic factors, including gender, race, ethnicity, social class, culture, etc. (Chen, H. & Volpe, R. P., 1998). However, this review focuses solely on the influence of gender on socialization. Acknowledging that the connections made in this review may not apply to certain demographic groups or regions is essential. A separate limitation is the lack of longitudinal research on women’s early socialization and its long-term effects on financial behavior. Future research can help identify and confirm this link through longitudinal studies. There are also potential biases due to the data collection methods, which consist of self-reports in the literature reviewed. While this review revealed valuable information on gendered financial socialization, these limitations emphasize the need for further research to understand the multiple factors intertwining to shape financial literacy entirely.

Implications

The findings of this review suggest several implications for education, policy, and future research. The studies have shown that financial education is critical, specifically early financial education. Women worldwide lack financial literacy due to a lack of financial education, leading to a greater gender wealth gap. Moving forward, policymakers should consider early financial education as a critical element and effective method of promoting gender equity in the long term (Bae, 2023). The empirical tests for the effect of financial education on financial literacy suggest that women who receive early financial education to improve their financial literacy can better understand the compounding effect of interest rates on loans, portfolio diversification, and mortgage payments. It was also revealed that early financial education on financial behavior positively correlates with women’s increased participation in the stock market, insurance activities, and savings habits (Bae, 2023).

Looking forward, linguistic relativity theory should be considered when discussing societal changes related to gendered language and its influence on financial confidence and participation. The use of gendered verbiage and gender-differentiated pronouns when talking about careers, specifically in finance and investing, can foster the development of internalized sexism in children through exposure to societal stereotypes (Hechavarría et al., 2017; Boroditsky, Schmidt, & Phillips, 2003). Research suggests that the implicit use of gendered-verbiage can lead girls to internalize the idea that investing and financial fields are not meant for them, specifically when considering their gender identity. This internalization may contribute to long-term disengagement from a girl’s future financial opportunities. Suppose changes are made as a society in terms of the use of gendered verbiage by shifting towards more inclusive language, where feminine pronouns are used more to describe professions. In that case, this may help reduce the gender gap in financial literacy and investment behavior.

Conclusion

This literature review demonstrates that early gendered messaging plays an important role in shaping women’s financial literacy development and investment behaviors throughout the life course. By synthesizing research on internalized sexism, parental socialization, linguistic structure, and financial confidence, this review emphasizes how early social environments contribute to persistent gender differences in financial behavior. Understanding these developmental pathways provides a foundation for future research and intervention strategies aimed at reducing the financial gender gap.

Citations

Agnew, S., & Cameron-Agnew, T. (2015). The influence of consumer socialisation in the home on gender differences in financial literacy. International Journal of Consumer Studies, 39(6), 630–638. https://doi.org/10.1111/ijcs.12179

Andersson, M. A., & McSwain, A. N. (2025). Internalized sexism and well-being in the United States. Journal of Health and Social Behavior, 0(0). https://doi.org/10.1177/00221465241305586

Bae, K., Jang, G., Kang, H., & Tan, P. (2022). Early financial education, financial literacy, and gender equity in finance. Asia-Pacific Journal of Financial Studies, 51(3), 372–400. https://doi.org/10.1111/ajfs.12378

Barber, B. M., & Odean, T. (2001). Boys will be boys: Gender, overconfidence, and common stock investment. The Quarterly Journal of Economics, 116(1), 261–292. https://doi.org/10.1162/003355301556400

Bayyurt, N., Karışık, V., & Coskun, A. (2013). Gender differences in investment preferences. ResearchGate. https://www.researchgate.net/publication/277313389_Gender_Differences_in_Investment_Preferences

Bearman, S., & Amrhein, M. (2014). Girls, women, and internalized sexism. In E. J. R. David (Ed.), Internalized oppression: The psychology of marginalized groups (pp. 191–225). Springer.

Bhattacharya, U., Kumar, A., Visaria, S., & Zhao, J. (2024). Do women receive worse financial advice? The Journal of Finance, 79(5), 3261–3307. https://doi.org/10.1111/jofi.13366

Bishop, A. (2017). Intergenerational transmission of gender ideology: The unique associations of parental gender ideology and gendered behavior with adolescents’ gender beliefs (Master’s thesis, Colorado State University).

Blaschke, J. (2022). Gender differences in financial literacy among teenagers: Can confidence bridge the gap? Cogent Economics & Finance, 10(1). https://doi.org/10.1080/23322039.2022.2144328

Boroditsky, L., Schmidt, L. A., & Phillips, W. (2003). Sex, syntax, and semantics. In D. Gentner & S. Goldin-Meadow (Eds.), Language in mind: Advances in the study of language and thought (pp. 61–79). MIT Press.

Bozkur, B., & Arıcı Şahin, F. (2022). Relationships among traditional gender roles, acceptance of external influence and self-alienation: The mediator role of internalized sexism. International Journal of Progressive Education, 18(4), 43–53. https://doi.org/10.29329/ijpe.2022.459.4

Bucher-Koenen, T., Lusardi, A., Alessie, R., & Van Rooij, M. (2016). How financially literate are women? An overview and new insights. Journal of Consumer Affairs, 51(2), 255–283. https://doi.org/10.1111/joca.12121

Cameron, D. (1998). Gender, language, and discourse: A review essay. Signs, 23(4), 945–973.

Chambers, R. G., Asarta, C. J., & Farley-Ripple, E. (2019). Gender, parental characteristics, and financial knowledge of high school students: Evidence from multicountry data. Journal of Financial Counseling and Planning, 30(1), 97–109. https://doi.org/10.1891/1053-3073.30.1.97

Chen, H., & Volpe, R. P. (1998). An analysis of personal financial literacy among college students. Financial Services Review, 7(2), 107–128. https://doi.org/10.1016/S1057-0810(99)80006-7

Clarke, M. C. (2005). The acquisition of family financial roles and responsibilities. Family and Consumer Sciences Research Journal, 33(4), 321–340. https://doi.org/10.1177/1077727X04274117

Croft, A., Schmader, T., & Block, K. (2015). An underexamined inequality: Cultural and psychological barriers to men’s engagement with communal roles. Personality and Social Psychology Review, 19(4), 343–370.

Cudd, A. E., & Jones, L. E. (2005). Sexism. In R. G. Frey & C. H. Wellman (Eds.), A companion to applied ethics (pp. 102–117). Blackwell.

Cupák, A., Fessler, P., & Schneebaum, A. (2020). Gender differences in risky asset behavior: The importance of self-confidence and financial literacy. Finance Research Letters, 42, 101880. https://doi.org/10.1016/j.frl.2020.101880

David, E. J. R. (2014). Internalized oppression: The psychology of marginalized groups. Springer.

Edwards, R., Allen, M. W., & Hayhoe, C. R. (2007). Financial attitudes and family communication about students’ finances: The role of sex differences. Communication Reports, 20(2), 90–100. https://doi.org/10.1080/08934210701643719

Etgar, S., Oestreicher-Singer, G., & Yahav, I. (2024). Implicit bias in LLMs: Bias in financial advice based on implied gender. Tel Aviv University. https://coller.tau.ac.il/sites/coller.tau.ac.il/files/media_server/Recanati/management/safra/galo.pdf

Fan, L., Lim, H., & Lee, J. M. (2021). Young adults’ financial advice-seeking behavior: The roles of parental financial socialization. Family Relations, 71(3), 1226–1246. https://doi.org/10.1111/fare.12625

Gill, A., & Biger, N. (2009). Gender differences and factors that affect stock investment decision of Western Canadian investors. International Journal of Behavioural Accounting and Finance, 1(2), 135. https://doi.org/10.1504/IJBAF.2009.027449

Glick, P., & Fiske, S. T. (1997). Hostile and benevolent sexism: Measuring ambivalent sexist attitudes toward women. Psychology of Women Quarterly, 21(1), 119–135. https://doi.org/10.1111/j.1471-6402.1997.tb00104.x